The Initiation and Approval process helps you to start off your project on the right foot. Find out how you can achieve it in 10 steps.

Project managers are accountable for many decisions that affect the research and development (R&D), testing, design, operations, and even the overall growth of the company. A good product manager should leverage the Initiation and Approval process of projects to examine the associated risks and mitigate them right at the start. Such a process is even more crucial for big projects that may affect the company's growth and its survival.

What kind of products/projects need Initiation and Approval?

It depends on the size and risk of the project.

The Ansoff Matrix can help us decide whether a project needs Initiation and Approval. The market here means customer group. From the table below, we can conclude that projects involving new markets, or a new type of product are high risk and therefore need Initiation and Approval. Existing products for the existing market do not need such a process. However, if it is for a large project (requiring more than 30 man-days), Initiation and Approval is needed.

Initiation & Approval of a B2B product in 10 steps

Step 1: Industry Value Chain Research

Industry value chain research provides a complete understanding of the industry, and it happens before customer research and competitor research. The research can be conducted through analyzing macro data, microdata, industry and consumer segments, as well as business processes of some typical companies in the industry.

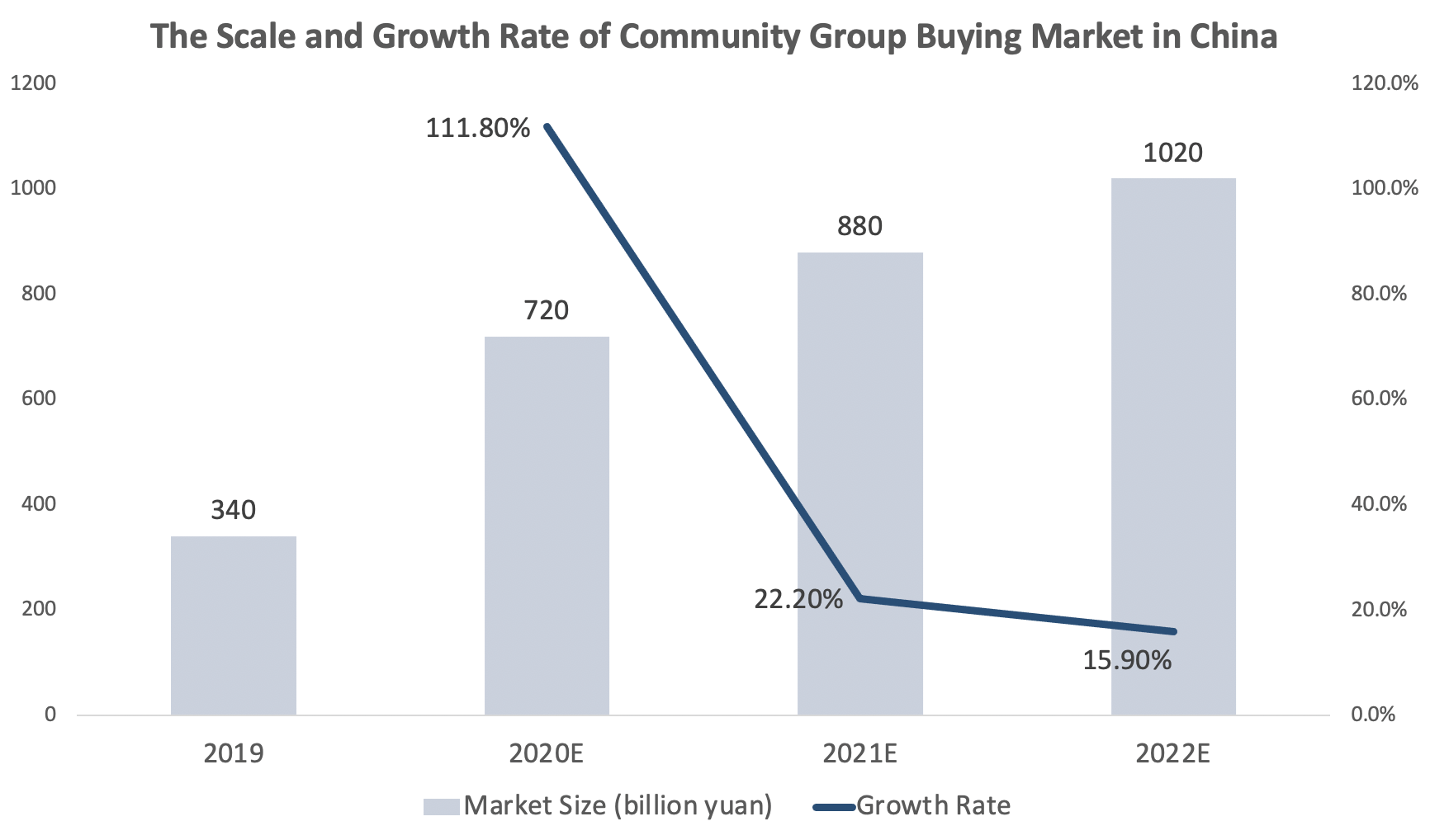

Through macro data analysis, we can analyze the Political, Economic, Socio-Cultural, and Technological (PEST) changes in the industry. Microdata analysis provides deeper insights into customer groups, markets, channels, operations, marketing strategies, and purchase orders. Analyzing each sector of the industry helps us understand where the company stands in the process flow and what service it provides. Take the B2C e-commerce export industry in China as an example.

Step 2: Customer Journey Analysis

A product manager must have a perfect understanding of customers' existing problems and business processes. It is essential to closely examine how the customer does business, or even work at the customer’s site for some time. This will allow us to identify their pain points, the software they use, and other details instead of making assumptions based on secondary information. Without a thorough understanding of a customer’s current business operations, there will never be a practical product.

Step 3: Customer Needs Analysis

Through a customer needs analysis, we can identify what motivates different types of customers to buy a product or service based on differing needs. This allows us to map out the attributes and benefits relevant to each customer profile. Afterwards, we can get to the bottom of “who and what” – finding out what the different customer profiles want, their willingness to pay, or how many of them are already existing customers.

It is important to segment customer types according to distinct needs and creates a detailed customer profile for further insights. How many different customer profiles are there? What are the sizes of each group? Which of them are more able and willing to pay? Answering these questions allows us to focus on potential customer profiles that are worth looking into.

Step 4: Competitive Analysis

Competitive Analysis illustrates the strengths and weaknesses of a product compared to its competitors. We can use this method to identify opportunities to outperform other competitors.

Studying the competitors’ websites, social media, and the product itself forms the foundation. For deeper insights, always learn about the distributor and direct user feedback, as well as the investment and financing of competing products.

Step 5: Exploring Opportunities

Now that you have a thorough view of the industry, customers, and competitors, it is time to exploit market opportunities. What is considered an opportunity?

An opportunity is when you can identify clear customer needs that are aligned with the competitiveness of your company. Generally, you can find opportunities from the market trend or pain points in customers’ business operations.

Step 6: Product Planning

Product planning, which includes the product architecture, functionality, and differentiating factors that make it stand out in the market, should be an ongoing process instead of a one-off consultation.

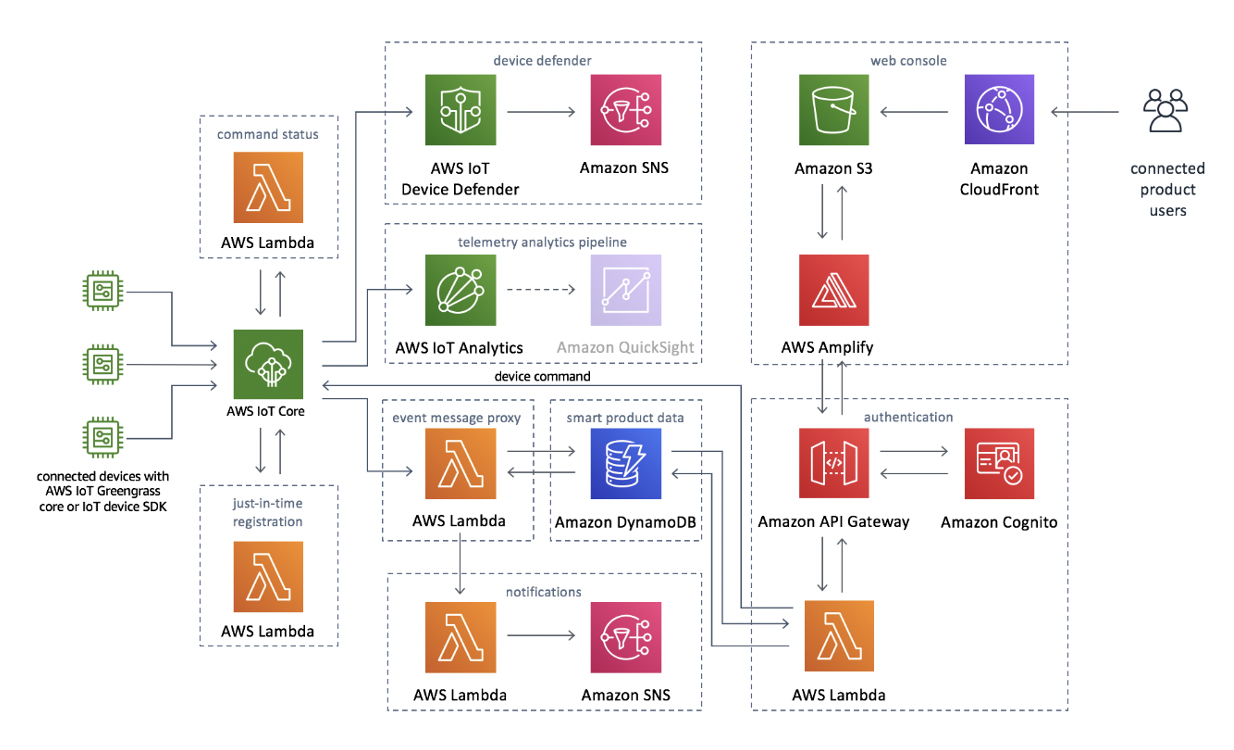

The diagram below is an example of Amazon Web Services (AWS) product planning (for reference only):

Step 7: Business Model

While product planning is about figuring out what to do, the business model focuses on monetization and commercial value – something the company's senior management cares about. What kind of services do you provide? Who is receiving the services? What is the monetization process? How to stand out among your competitors? Answer the following questions to understand your business model.

Step 8: Value Analysis

Value analysis is based on the business model, but it addresses a higher-level question: why are we doing it? Explain your company’s customer value, business value, and strategic value for both the short-term and long-term.

Step 9: Project Planning

After answering the questions of what and why the next step is project planning. This includes product planning, product operation strategies, and monetization timeline. Try to make each stage of the development independent and each version of the product available for trial. Generally, larger projects take longer to develop and implement. There will be more risks if customers are not involved in each stage of testing. Project planning provides an overall view on manpower, timeline, delivery scope, and quality requirements. The table below is a project planning template for your reference.

One page plan for project basics by KigoSpace.com

Step 10: Risk Management

The last step of Initiation and Approval is risk management. This step estimates, identifies, analyzes, and responds to any involved risks. Put together a list of potential risks and give solutions to each of them before starting the next phase. For each major risk identified during the development process, create a plan to mitigate it based on prioritization.